In the past few months we’ve added more new babies to our household than credit cards. While babies are cute and cuddly, they tend to increase household costs. Credit cards, on the other hand, are hard and plastic, but they can be worth hundreds of dollars in value. A few days ago we got 4 new arrivals at the house and none of them was cuddly…but they were all valuable. Here’s a breakdown of our latest round of card apps:

Nicoleen:

Citi Hilton HHonors Reserve

- $95 annual fee due up-front

- Two free weekend night certificates for any Hilton property worldwide after spending $2.5k in the first 4 months

- 10x points earned on Hilton properties purchases, 5x on travel, 3x on all other purchases

- HHonors gold status when card account is active

Ross:

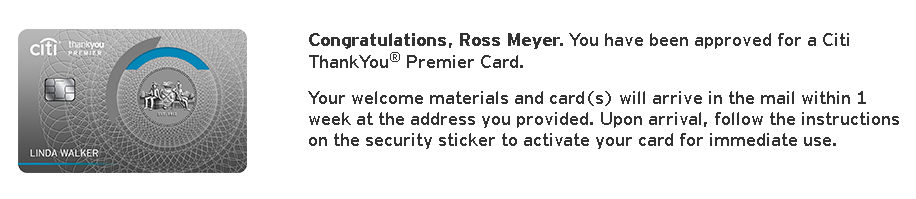

Citi Thank-You Premier

- $95 annual fee waived the first year

- 50,000 Thank-You points after spending $3k in the first 3 months (worth a minimum of $500)

- 3x points earned on travel and gas, 2x on dining and entertainment, 1x on all other purchases

And we each got:

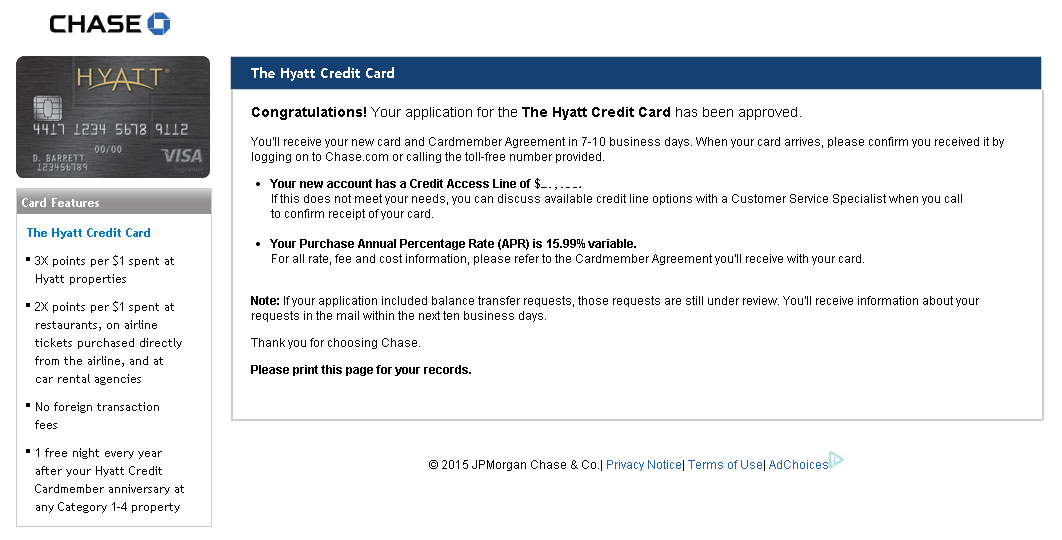

Chase Hyatt Visa

- $75 annual fee waived the first year

- Two free night certificates for any Hyatt property worldwide after spending $1k in the first 3 months

- 5,000 Gold Passport points for adding an authorized user

- 3x points earned on Hyatt properties purchases, 2x on dining, airfare and car rental, 1x on all other purchases

- Anniversary free night certificate good at any Hyatt property, category 1-4.

The Rationale:

The Chase Hyatt card was the driving force behind our choice of cards for this round of apps. The Hyatt card has been on my radar for a while because of the incredible value potential in the two free night certificates per card. A pair of these cards could potentially be worth almost $4,000 in lodging. Two nights at a fancy hotel hardly constitutes vacation though, so the obvious tactic to maximize this card is for both of us each get our own card; then we’d have 4 free nights.

We have always planned on both getting the Chase Hyatt card at the same time, but it’s still a stretch to call 4 free nights a vacation. The other major card offering free nights is the Citi Hilton Reserve, with its two free weekend night initial spend bonus. If we could find a vacation-worthy Hyatt property in close proximity to a vacation-worthy Hilton property, we could get a 6 night vacation split between two luxury properties, for the $95 annual fee paid one credit card! I earned the bonus on the Citi Hilton Reserve last year so I was ineligible for the bonus again. (Furthermore, the most I would have been able to add to the proposed vacation would be one free Hilton night, since the certificates are only good for Fri/Sat/Sun nights.)

I always try to apply for only one card per issuing bank per app-o-rama. We both had the Chase slot filled with the Hyatt card. Nicoleen filled the Citi slot with the Hilton Reserve. But I still needed a second application, and Citi had some good card options. I settled on the Thank-You Premier with it’s 50,000 point bonus.

It seems like a pretty good plan. We have a specific redemption idea in mind for the hotel free nights, all three hotel cards compliment each other, and the Citi Thank-You will add some points to the general pool for when it comes time to find airfare. So this was a hybrid of both basic strategies I wrote about in this post.

Application set-up and results

Chase has been getting stingy and seemingly capricious about approving credit card applications lately. This is concretely seen in their Ultimate Rewards earning cards, which they will now outright deny to anyone who has had 5+ new accounts with any issuer in the past 24 months. But there have also been an increasing number of denial reports with co-branded Chase cards. i didn’t want to take any chances because the Hyatt free night certificates are only good for a year, so it was crucial that Nicoleen and I have as much time overlap in certificates as possible.

To prepare for the Chase application I requested credit line decreases in two of my Chase cards: my Sapphire Preferred from $11.1k to $5k; and my IHG card from $9k to $4k. I made both requests via Secure Message a few days apart, and both credit lines were lowered within a day of the request. I had closed my United Mileage Plus Explorer account with a $9k credit limit back in April, so I figured between the 3 credit line decreases I would have plenty of overhead left with Chase. The thought was to remove “maxed out credit limit” as a possible reason for denial. It worked!

Nicoleen had also recently cancelled her United card and she has fewer Chase accounts than I, so we didn’t do anything in particular before her application. Our luck continued as she was instantly approved too!

In my experience applying for Citi cards is much more of a push-over. The only time I was not instantly approved for a Citi card was when I got “pending” with a business card. The call to the reconsideration line for that card was quick and painless.

So with nothing more than fingers crossed we applied for our respective Citi cards and experienced the always welcome instant approval notices!

Within a week we had all 4 cards in our possession:

Minimum Spend and Redemption Plans

With a specific goal to use 3 cards’ worth of hotel certificates on a single trip, some tactics need to be employed to maximize the probability of everything lining up correctly. Number one is to get all the hotel certificates ASAP. This means getting the spends on the Hyatt cards and Hilton card taken care of.

The Chase Hyatt cards’ spends are easy, with only $1000 per card to get the certificates issued. AND they are issued as soon as the minimum spend has been met; not after the statement closes like with the Hilton certificates. Furthermore, getting these done before the Hilton is tactically important because with 4 contiguous free nights we could still cobble together a vacation. But if we got the Hilton certificates and booked a room, only to have the nearby Hyatt property become booked while we were still working on the Hyatt card spends, we would have to regroup and make different plans. So . . . Hyatt cards first.

Since there are many airlines that fly to our destination (Maui) but only one Hilton property we have in mind, Nicoleen’s Hilton Reserve gets the next highest priority for our card usage. While the 50,000 bonus Thank-You points would be a nice help to our plans, they aren’t as critical as the Hilton free night certificates, so the Citi Thank-You Premier will be the last bonus spend we complete.

In my next post it’s on to the fun part: sign-up bonus bonus redemption plans!