I sometimes get comments related to the fact that some of the deals and tactics I outline on this site are not available in certain geographic areas. While I can’t promise to cover all deals/promotions available everywhere in the world, I can tell you I feel your pain.

The Problem

No awesome in-branch-only credit card offers for me! (I live in Minnesota)

On more than one occasion I have seen credit card offers only available at Chase branches, but I live in a state (Minnesota) where there are no Chase branch locations. I once tried to execute a currency trading tip I was given and I ran into roadblock after roadblock. It turns out the type of trade I wanted to do is not allowed using U.S. brokerages. These and other are other examples of tactics I am unable to employ due to where I live, and it’s frustrating every time.

I’m sure many of you feel the same frustration. Two of the free money tactics I promote on this site involve retailers only present in the Midwest (Super America and Menards). And if you live outside the U.S you’re out of luck on most of the credit card advice on this site. The credit card deals I post about are generally limited to U.S. customers.

Menards store locations are concentrated in the Great Lakes region.

Good deals are everywhere – The strategy

The geography of available coupon deals, credit card promotions, and other savings tactics is much like the timing of credit card sign-ups: you’ll win some and you’ll lose some. The good thing is that the overall strategy can easily be exported to other regions with different tactical opportunities. Once you start learning how to evaluate deals and sort through the spam, you’ll find it’s easy to spot what might be worth doing and what isn’t.

I don’t claim to be a clearinghouse of information on the best deals and offer around the country, but I welcome tips my readers have about similar tactics available where they live. E-mail me or comment on the relevant posts when you know of non-Midwest, regionally specific tactics. Let’s band together to capture and create value across the nation globe!

Adam Sandler’s character in “Punch Drunk Love” working on hoarding 1,000,000 miles through a loophole in a product label promotion. He’d better spend some before the next devaluation!

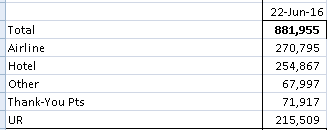

In last week’s update I mentioned that I recently realized I had close to 1 million points and miles in various airline, hotel, and credit card programs. Being a points millionaire might seem like a fun title to have, but in fact it’s dangerous. No, I don’t mean you would need a bodyguard and a home security system; I mean your huge points and miles balances are a liability because they are only worth something when you redeem them, and redeeming them gets worth less and less as time goes by.

Too many points saved up? Maybe . . .

Read on to learn the three possible downsides to building up an oversized point and mile portfolio.

1. Devaluations

Frequent flyer and hotel rewards programs routinely devalue their points by raising the average number of points needed for a given flight or hotel stay. This is their way of accounting for inflation. If the dollar’s real value is decreasing by 3.1% per year (the average over several decades), it means we’re spending 3.1% more nominal dollars per year. If every dollar we spend on a co-branded credit card earns us x points or miles, we are getting more and more redemptive power as time goes by. At the same time, the hotels’ and the airlines’ real cost of granting you the free flights and hotel nights stays the same. To account for this they raise the points needed for their redemptions.

Then there’s the unpleasant but unavoidable fact that websites like mine, other blogs, and forums like Flyertalk (along with the general increase in communication since these programs were started) are making these programs less lucrative for the airlines, hotel chains, and credit card companies. As more and more people learn how to maximize the value of these programs and work every angle down to the finest detail, the companies have to push back to maintain their profits.

There are a variety of factors that cause points and miles devaluations, but it’s a fact that they will continue to occur. No one should be surprised by this. I agree with most of the big time bloggers on the subject, where the consensus is: It’s ok to devalue your points, but don’t try to hide it from your customers. A recent Southwest devaluation seems to have done just that.

Points and miles gradually lose their value over time, so spending them sooner rather than later is one important tactic to maximize their value.

2. Mergers

Last year U.S. Airways was absorbed into American Airlines. Earlier this year it was announced that Marriott will be purchasing Starwood. Each frequent flier and preferred guest program have their unique benefits and redemption tricks. When mergers happen, these program nuances are usually lost. Sure, you may gain some new program benefits when you lose others, but on the whole it seems like the new entity always manages to come out on top.

For example, Starwood is famous for its awesome redemption rates at hotels ($0.02 per point, compared to Hilton’s roughly $0.003 per point rate). The fate of everyone’s Starwood points after the Marriott merger is still unknown, but the travel community seems to be preparing for a net loss of value.

While mergers are usually known well in advance, putting all your eggs in one basket – a basket that may get dumped into another basket – is probably not the best idea.

3. Known or unknown transgressions (account closure risk)

This one is tough. Everyone has to formulate their own ethical code of conduct when dealing with credit card bonuses and points earning strategies. I personally play it pretty safe. I don’t get new cards every three months like clockwork, I’m not into blatant manufactured spending, and in general I try to play by the rules. Of course I explore the limits of the rules, but that’s the fun part! I get a lot of value from these programs and I don’t want to risk being blacklisted. In short, I don’t want the powers that be to like me; I want them to not even notice me.

Then there are those who play hard ball. People who spend thousands a month on manufactured spending. People who get authorized user cards for their dogs and cats to get the bonuses some cards offer. People who attempt tactics such as getting the bonus spend the first day they get a card, waiting for the bonus to post, and then cancelling the card before the first month’s bill closes to avoid paying an up-front annual fee.

These people really have to worry about the future of their stored points and miles!

It’s not unheard of for accounts to be summarily closed without warning. While many people who report such closures claim they’re completely innocent, I have a feeling most of them have done something to get on the radar of the credit card companies. Chase seems particularly ruthless toward program abusers. There is even a huge Flyertalk thread just for reports of Chase Ultimate Rewards accounts being wiped.

While most of these cases are probably warranted, I’m sure mistakes are sometimes made and unsuspecting decent folks have their points accounts obliterated without just cause. The fine print associated with these programs usually gives the bank total authority over your points accounts.

Even if you’re not playing with fire, the chance exists that you could fall out of disfavor with a bank or airline and lose all your stockpiled miles. Don’t take the chance . . .DON’T HOARD POINTS!

Chase is making the credit card game much more difficult. Starting some time in April, Chase will apply it’s 5/24 rule to new applications for all their co-branded and Ultimate Rewards earning credit cards (all their good cards). The 5/24 rule stands for 5 cards in 24 months, and means that if you have opened 5+ new credit card accounts at any bank in the past 24 months, you’ll be automatically denied for whichever Chase card you are applying for. Being added as an authorized user to someone else’s account also counts against your 5. All reports seem to indicate this is a hard and fast rule.

Such an ugly word…

The 5/24 rule is not exactly news. Reports of the new policy started appearing on Flyertalk’s Chase application forum last May. At the time it seemed like the rule only applied to Ultimate Rewards earning personal cards. This month the rule also kicked in for the Ink Plus, Chase’s Ultimate Rewards business card. Next month all relevant Chase cards will be affected.

IMPORTANT NOTE: ValueTactics reader Nidakeed reports having been denied a Chase Sapphire Preferred due to a nuance of the 5/24 rule I hadn’t previously seen reported. Apparently Chase counts the entire month of your card approvals in their month tallying. For example, if the card approval that puts you over the limit occurred on February 15th two years ago, you have to wait until March 1st to apply for the Chase card. If you apply on February 25th, Chase will see that your 5th card was approved in February and still deny your application for violating the 5/24 rule because the approval happened in the same calendar month as your current application.

How bad is the 5/24 rule?

This move by Chase is definitely a game changer, but how much it affects you depends on where you are in your credit card career. For those just starting out, there’s still time to adjust your strategy (more on that below) to minimize the impact.

For those who are playing the game full steam ahead and managing to get 10+ new cards per year, there’s a hard choice to make: either slow down your card applications to under 5 every 24 months, or completely eliminate Chase cards from your suite of regular applications. The former option drastically reduces your annual bonus point accumulation. The latter option disqualifies you from some of the best cards out there (many are from Chase) and severely reduces your accumulation potential for Chase Ultimate Rewards points, widely viewed as the most valuable and versatile points out there.

For those just starting out, you still have the opportunity to get in one or two good rounds that include cards from Chase before you hit the limit. Refer to my article on deciding on which cards to get and keep this new rule in mind. Specifically, I would recommend getting the Chase Sapphire Preferred (good for 59k+ Ultimate Rewards points just for making the minimum spend) and/or the Chase United MileagePlus Explorer (30k mile bonus as of this writing but wait until it get jacked up to 50k, which it does routinely). If you own a business or make side income that could be presented as a business, I recommend the Chase United Business card (as of this writing, a 50k mile bonus), and/or the Chase Ink Plus (60,000 Ultimate Reward points bonus). After you hit the 5 card limit in your first two years, you’ll have to decide how to proceed (see the next paragraph).

For those who are somewhere in the middle it’s time to reassess your current strategy. If you’ve been at it a while but at a slower pace, you have a decision to make. Do you want to slow way down on your card application rate to keep Chase cards available to you, OR do you want to have the freedom to apply for any card whenever the good promotions appear, but risk losing Chase as an option? Of course if you have already gotten the bonuses for the best Chase cards (see those listed in the preceding paragraph), this decision might be a bit easier considering you’re already probably waiting for the 2 year Chase bonus timer on getting each card’s bonus again.

5 card limit in 2 years — 5 cards on the Chase credit card homepage. Coincidence? ……yes.

Tactics to consider

Regardless of your situation, there are a few tactical considerations you need to incorporate into your overall card strategy:

If you’re currently under the 5 cards in 24 months limit the #1 smart thing to do is to front load Chase cards in your plan. Get the best 2-3 Chase cards in your first 2 rounds of apps to ensure you can get these bonuses before you hit the 5/24 limit.

Some cards offer bonus points for adding an authorized user (such as the Chase Hyatt and Chase Sapphire Preferred, each offering 5,000 points for adding an authorized user and making one purchase on that card.) All reports indicate that Chase counts being added as an authorized user against your 5 cards. If you are adding an authorized user just for the bonus, consider getting the card for a minor child or another trustworthy relative, as opposed to a spouse who may want to incorporate Chase into their own strategy. Make sure you get permission from the person. Also, make sure the authorized user is a real person or you risk having your account closed. There are many stories of people getting cards for their dog or cat and never having a problem, but I personally wouldn’t risk it.

Conclusion

The Chase 5/24 rule is going into effect for all their worthwhile cards starting in April. It isn’t the end of the world but it’s nothing to ignore either. Those of you just starting out, who currently have fewer than 5 new card approvals in the past 24 months, are best situated to avoid the ramifications of this new rule. Moving any Chase cards you may be considering to the front of your card application schedule is the primary tactic to mitigate the new rule’s restrictions. For those of you who are currently exceeding the 5 cards in 24 months rule, it’s time to take a close look at your strategy.

In the past few months we’ve added more new babies to our household than credit cards. While babies are cute and cuddly, they tend to increase household costs. Credit cards, on the other hand, are hard and plastic, but they can be worth hundreds of dollars in value. A few days ago we got 4 new arrivals at the house and none of them was cuddly…but they were all valuable. Here’s a breakdown of our latest round of card apps:

Nicoleen: Citi Hilton HHonors Reserve

$95 annual feedue up-front

Two free weekend night certificates for any Hilton property worldwide after spending $2.5k in the first 4 months

10x points earned on Hilton properties purchases, 5x on travel, 3x on all other purchases

HHonors gold status when card account is active

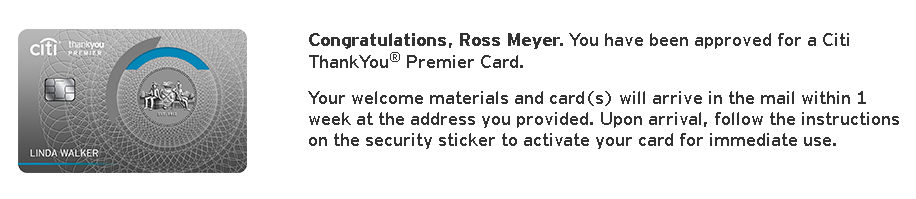

Ross: Citi Thank-You Premier

$95 annual feewaived the first year

50,000 Thank-You points after spending $3k in the first 3 months (worth a minimum of $500)

3x points earned on travel and gas, 2x on dining and entertainment, 1x on all other purchases

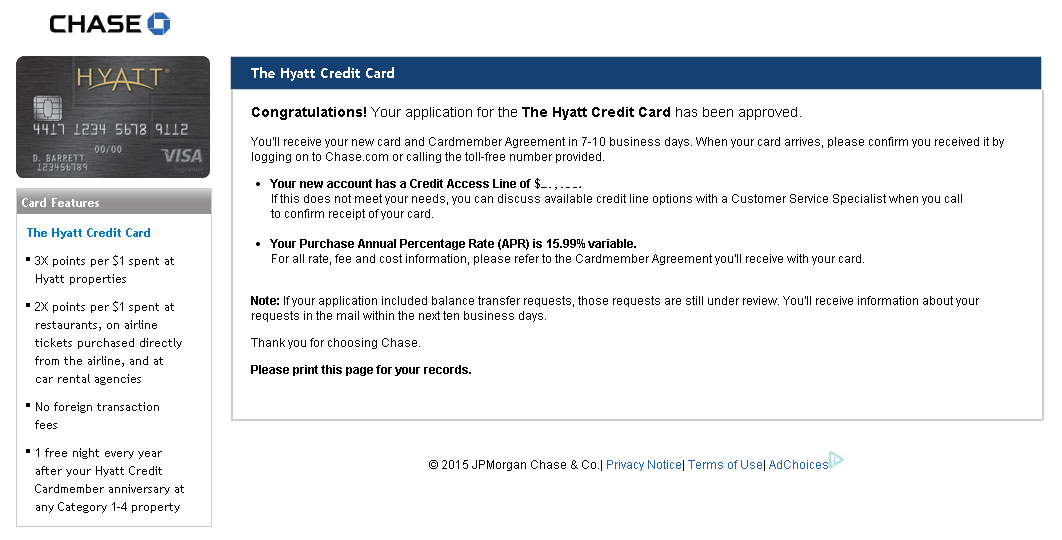

And we each got: Chase Hyatt Visa

$75 annual feewaived the first year

Two free night certificates for any Hyatt property worldwide after spending $1k in the first 3 months

5,000 Gold Passport points for adding an authorized user

3x points earned on Hyatt properties purchases, 2x on dining, airfare and car rental, 1x on all other purchases

Anniversary free night certificate good at any Hyatt property, category 1-4.

The Rationale:

The Chase Hyatt card was the driving force behind our choice of cards for this round of apps. The Hyatt card has been on my radar for a while because of the incredible value potential in the two free night certificates per card. A pair of these cards could potentially be worth almost $4,000 in lodging. Two nights at a fancy hotel hardly constitutes vacation though, so the obvious tactic to maximize this card is for both of us each get our own card; then we’d have 4 free nights.

We have always planned on both getting the Chase Hyatt card at the same time, but it’s still a stretch to call 4 free nights a vacation. The other major card offering free nights is the Citi Hilton Reserve, with its two free weekend night initial spend bonus. If we could find a vacation-worthy Hyatt property in close proximity to a vacation-worthy Hilton property, we could get a 6 night vacation split between two luxury properties, for the $95 annual fee paid one credit card! I earned the bonus on the Citi Hilton Reserve last year so I was ineligible for the bonus again. (Furthermore, the most I would have been able to add to the proposed vacation would be one free Hilton night, since the certificates are only good for Fri/Sat/Sun nights.)

I always try to apply for only one card per issuing bank per app-o-rama. We both had the Chase slot filled with the Hyatt card. Nicoleen filled the Citi slot with the Hilton Reserve. But I still needed a second application, and Citi had some good card options. I settled on the Thank-You Premier with it’s 50,000 point bonus.

It seems like a pretty good plan. We have a specific redemption idea in mind for the hotel free nights, all three hotel cards compliment each other, and the Citi Thank-You will add some points to the general pool for when it comes time to find airfare. So this was a hybrid of both basic strategies I wrote about in this post.

Application set-up and results

Chase has been getting stingy and seemingly capricious about approving credit card applications lately. This is concretely seen in their Ultimate Rewards earning cards, which they will now outright deny to anyone who has had 5+ new accounts with any issuer in the past 24 months. But there have also been an increasing number of denial reports with co-branded Chase cards. i didn’t want to take any chances because the Hyatt free night certificates are only good for a year, so it was crucial that Nicoleen and I have as much time overlap in certificates as possible.

To prepare for the Chase application I requested credit line decreases in two of my Chase cards: my Sapphire Preferred from $11.1k to $5k; and my IHG card from $9k to $4k. I made both requests via Secure Message a few days apart, and both credit lines were lowered within a day of the request. I had closed my United Mileage Plus Explorer account with a $9k credit limit back in April, so I figured between the 3 credit line decreases I would have plenty of overhead left with Chase. The thought was to remove “maxed out credit limit” as a possible reason for denial. It worked!

Nicoleen had also recently cancelled her United card and she has fewer Chase accounts than I, so we didn’t do anything in particular before her application. Our luck continued as she was instantly approved too!

In my experience applying for Citi cards is much more of a push-over. The only time I was not instantly approved for a Citi card was when I got “pending” with a business card. The call to the reconsideration line for that card was quick and painless.

So with nothing more than fingers crossed we applied for our respective Citi cards and experienced the always welcomeinstant approval notices!

Within a week we had all 4 cards in our possession:

Minimum Spend and Redemption Plans

With a specific goal to use 3 cards’ worth of hotel certificates on a single trip, some tactics need to be employed to maximize the probability of everything lining up correctly. Number one is to get all the hotel certificates ASAP. This means getting the spends on the Hyatt cards and Hilton card taken care of.

The Chase Hyatt cards’ spends are easy, with only $1000 per card to get the certificates issued. AND they are issued as soon as the minimum spend has been met; not after the statement closes like with the Hilton certificates. Furthermore, getting these done before the Hilton is tactically important because with 4 contiguous free nights we could still cobble together a vacation. But if we got the Hilton certificates and booked a room, only to have the nearby Hyatt property become booked while we were still working on the Hyatt card spends, we would have to regroup and make different plans. So . . . Hyatt cards first.

Since there are many airlines that fly to our destination (Maui) but only one Hilton property we have in mind, Nicoleen’s Hilton Reserve gets the next highest priority for our card usage. While the 50,000 bonus Thank-You points would be a nice help to our plans, they aren’t as critical as the Hilton free night certificates, so the Citi Thank-You Premier will be the last bonus spend we complete.

In my next post it’s on to the fun part: sign-up bonus bonus redemption plans!

Around the time of Nicoleen’s and my anniversary trip to Europe this summer, valuetactics.com got quite a lot of attention from Nicoleen’s facebook crowd. Many friends and relatives asked Nicoleen or me how we landed such good deals on the flights, hotel, and other trip expenses. If you want more detailed on the trip itself, check out this post outlining our itinerary.

If you’re one of those who are just curious how we did it (and maybe are curious how you too can travel for free!) in this post I’ll briefly outline the strategy we use to accumulate points and plan trips.

If you’re just starting out it’s helpful to adopt one of two strategies, to avoid accumulating what may turn out to be less than useful points.

Points and miles strategy #1: Goal first, then reverse.

If you have enough lead time, you can start with your desired travel plans and then work backwards to figure out which points and miles programs would be most useful to you, and which cards/offers are best at earning you those points or miles.

Here’s a hypothetical example to illustrate the thought process:

You and your spouse want to go to Park City, Utah, for a weekend skiing get-away in March. Your travel budget only covers lift tickets, dining, and bar tabs; so your airfare and lodging need to be free. You’re also very demanding about accommodations so you need to stay in a luxury resort.

You regularly read valuetactics.com, so you know the best way to get free luxury hotel stays with a few month’s notice is with either the Hilton HHonors Reserve card from Citi or the Hyatt card from Chase. Both cards offer 2 free nights as the sign-up bonus, but the Hilton free nights are only good on weekends – not a problem for your plans. (Others, like Chase’s IHG card, only offer free nights as an account anniversary award). If you and your spouse each get approved for your own cards, you have 4 free nights to redeem…more than sufficient for your weekend ski trip.

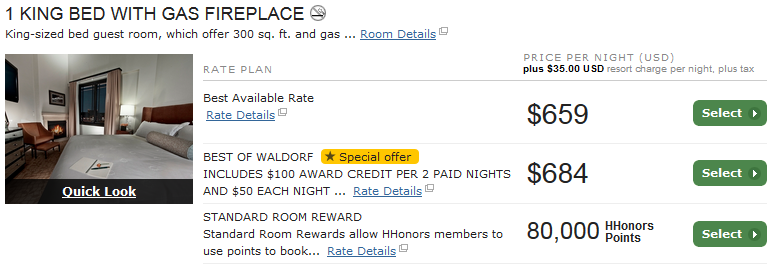

You check availability for March 18-21 at Hilton’s luxury resort in Park City, the Waldorf Astoria, and Hyatt’s, The Escala Lodge at Park City. Unfortunately, (for the sake of the example) you find that the Hyatt has no rooms available for reward certificate redemption. You check the Hilton website…your heart is pounding…will there be free rooms available? …yes! The Waldorf Astoria has plenty of reward certificate availability for that weekend! Looks like you’ll be applying for that Citi Hilton HHonors Reserve card.

The nice round number for the room’s award points price tells you it’s Hilton’s “standard” rate, meaning it’s available for a free night certificate redemption. A $659/night room for free…not a bad deal for taking a few minutes to apply for a card and make sure you hit the bonus spending!

The Waldorf Astoria in Park City, Utah

Ok, you have lodging covered. Now on to the free airfare. One of the keys to redeeming miles for flights is to find the “saver” level award availability. This is the discounted rate and will allow you to maximize the value of your airline miles. You can safely assume that at a given moment you have at least 2-3 options for cards that will earn you 40-50k airline miles or points that can be transferred to airline miles. So for this example, we’re trying to get two flights on our desired dates (March 18-21, 2016) for under 50,000 miles.

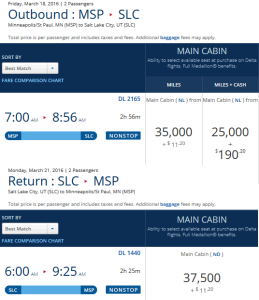

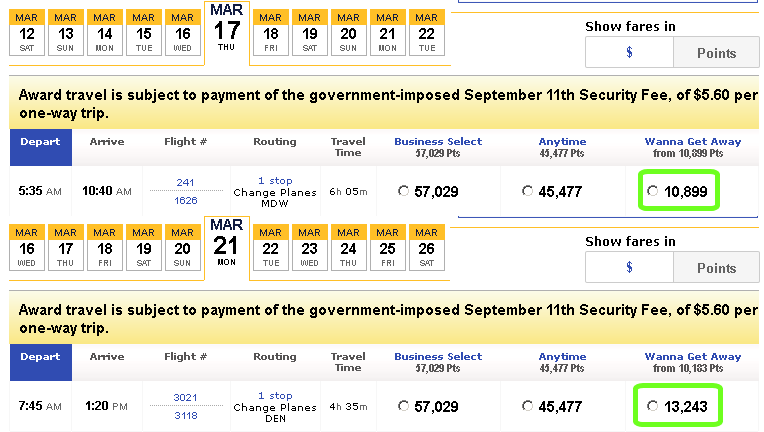

Let’s start with Minneapolis’s home town hero, Delta:

72.5k miles each; 135k miles for both of you…unacceptable.

On to United:

No saver level seats available for your dates.

How about American?

No dice.

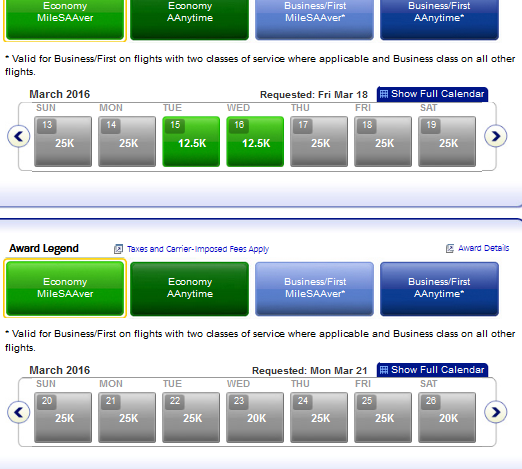

Southwest?

Now we’re talking! Two round trip flights for under 50k miles.

So how do you get 48,284 Southwest miles? Chase routinely (2x per year on average) jacks the sign-up bonus on their Southwest card up to 50,000 points. For this example, let’s say the 50k promotion just ended and the card comes with the standard 30k bonus. If you think you can get the bonus and quickly put another $18,284 in spending on the card to get the remaining points needed for your flights, then get the card! But remember, seat availability for flights is constantly changing so you probably want to get your seats booked ASAP, so trying to earn the remainder of the points organically might take a few months and your seats may be gone by then. Alternatively, you could each get the card and you’d be set, but I personally would never apply for a card that regularly has a jacked up bonus unless that promotion is running.

Is there a more streamline way to get 50k Southwest points fast? Why yes there is! Southwest happens to be a transfer partner of Chase Ultimate Rewards, meaning you can transfer UR points to your Southwest Rapid Rewards account at a 1:1 ratio, for free, instantly. There are several cards that earn Chase Ultimate Rewards including Chase Freedom, Sapphire Preferred, and Ink Plus business. After looking at all the benefits of these cards, you decide on the Sapphire preferred because the annual fee is waived the first year and it will earn you 49,000 UR points after meeting the bonus spend of $4k in 3 months. How convenient…that’s just what you need to transfer to Southwest and get your flights for free!

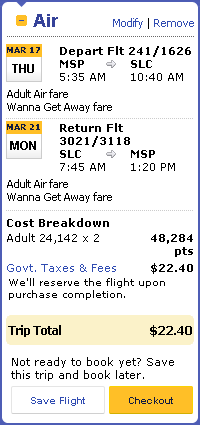

Let’s recap this example:

For applying for 3 credit cards between the two of you, paying the $95 annual fee on the two Hilton cards, and paying the $22.40 in fees to the airline, you are getting:

$2,082 worth of lodging to stay at the Waldorf Astoria for three nights

$809.92 worth of airfare on Southwest for two round trip tickets to SLC

That’s a total of $2892 in travel expenses for paying $202, doing some research, and spending 15 minutes to apply for a couple cards. A pretty good value if you ask me!

Points and miles strategy #2: Go all in!

If you don’t have a specific goal in mind, or would like the most flexibility when planning free travel, you could go all in and start accumulating as many points and miles as you can. This also means diversifying. Concentrating on highly versatile points is one facet of this strategy. Earning points in several different competing programs is another.

This strategy can be as valuable as you want it to be. The more carefully you plan and the more variables you look at, the more you can maximize your card applications. It would take a whole book to look at every facet of this strategy, but I will try to get you to think about some things to consider when getting into this game for the long haul.

Which cards can you “churn,” getting the bonus multiple times?

What is each card/bank’s particular quirks when considering applications?

What is your current credit score?

Which cards earn what kind of points?

Which points can transfer to which other programs?

Are there currently any “jacked up bonus” promotions running?

Do you have any travel plans on the horizon, a la strategy #1?

How can you group applications to maximize all of the above?

Other than the points bonus, what other benefits does each card have?

Can you stretch the benefits of a card by staggering them with your spouse?

Are there any weak points in your points and miles portfolios?

Which cards will soon be phased out?

As you can see, there is a lot of thought that can go into this game if you really want to maximize the value. Use this site and others to learn all you can about the different programs. I promise you, the learning curve is steep but short, and 90% of the confusion will go away by the time you earn your first card bonus and book your first trip with miles and points. If you have already been taking advantage of frequent flyer programs or hotel loyalty programs, you already have an advantage.

Of course you are not bound to one of these two strategies. Realistically everyone should incorporate elements of both into their planning, regardless of how much thought you put into that planning.

I hope this little primer helped some of you understand what to think about when deciding which card(s) to apply for. Now get out there and capture some value!